The Calculator Says I Can Retire at 39

A retirement calculator told me I can retire at 39.

According to it, I’m 100% on track.

Too good to be true! Or is it?

My Current Numbers

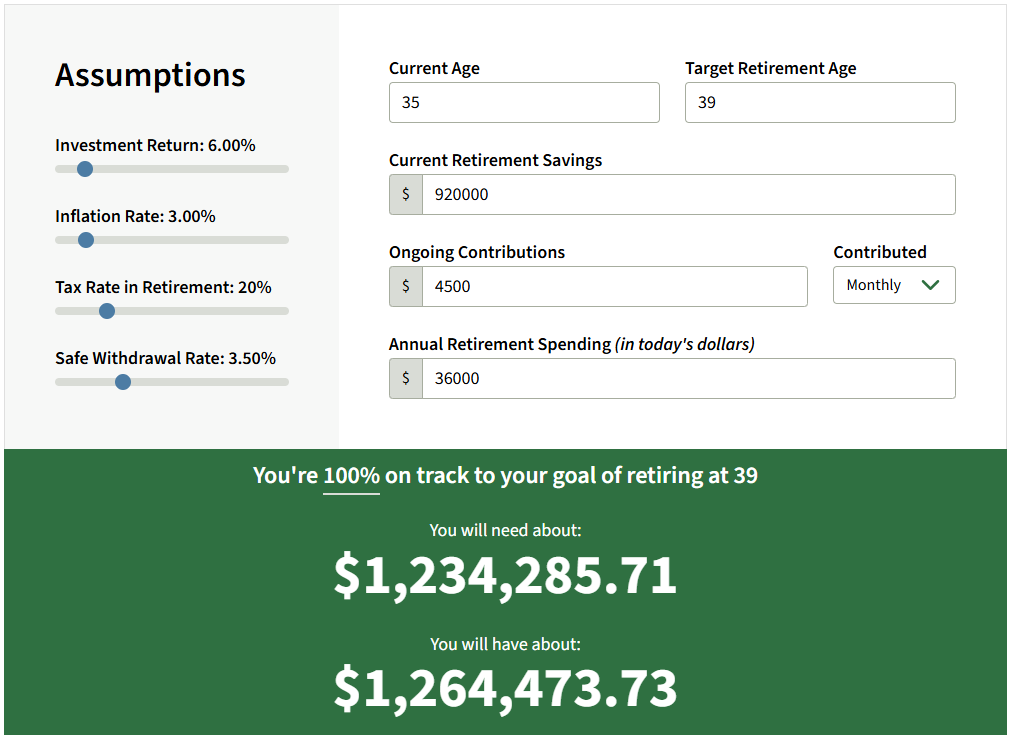

If you’re reading this post, you’ve probably tried punching in your numbers into an early retirement calculator to see how close you are to FIRE. I did the same thing, and the result showed that I’m 100% on track to retire by age 39.

The target number for early retirement is often said to be around $1.2M and at this rate, I don’t see any reason I wouldn’t reach it, unless something unexpected happens, like losing my job.

So on paper, everything looks fine.

My partner and I currently have the following accounts:

- Brokerage account

- 401(k)

- 2 Roth IRAs

- Solo 401(k)

- Multiple online checking/savings

We also own a condo. I’m leaning toward renting it out, but whether it will generate income or cost us money is still a big unknown.

In total, we have about $900K+ in financial assets.

Lower Cost of Living in Japan

Because we’re planning to move to Japan, our expected cost of living is much lower. On average, it’s around 270,000 JPY per month, which is roughly $1,700 USD. That’s less than half of what we currently spend!

To be conservative, I’m estimating $3,000 per month and a 6% investment return. I’ve also assumed a 20% tax rate in case of any unexpected Japanese taxes.

When I plug all of these numbers into a retirement calculator, the result looks promising:

Sounds great, right?

But Is It Actually True?

Let’s look at a few risks that could completely break this plan.

What If Financial Crisis Happens?

If you’re old enough, you probably remember what happened in 2008.

A major financial crisis caused the stock market to lose roughly half its value. Imagine having most of your net worth in stocks and waking up to see it cut in half overnight.

I made a quick python script to simulate 2008 crisis if I held my VTI stocks during those years, assuming that I’m still fully retired and withdraw 4% from the total asset value.

This simulation assumes I withdraw 4% of my portfolio each year based on its current value, and then apply that year’s market return.

Starting with $1.2M, the portfolio grows to about $1.33M by 2007. However, in 2008, it drops sharply to below $800K, which is a ~40% decline.

Because withdrawals are calculated as 4% of the current portfolio value, the amount I can withdraw also falls significantly during this period. In other words, my “income” drops at the same time the market does.

Even though the portfolio eventually recovers and surpasses its original value by 2013, that recovery isn’t smooth. For several years after the crash, both the portfolio value and withdrawal amounts remain lower than they would have been otherwise, because everything is compounding from a reduced base.

This illustrates an important point: even if you hit your target number (like $1.2M), a major downturn early in retirement can still materially impact your income for years.

That’s not just a theoretical risk. That’s my entire life plan on the line.

Bonds at Rescue?

This is why people often recommend shifting toward a more bond-heavy portfolio as you approach retirement.

Bonds typically have lower returns than stocks, but they tend to be less volatile and provide more stability.

But even that doesn’t completely solve the problem.

Looking back at 2008, it took about five years for the stock market to recover to its previous level.

So the question is:

Would you have avoided the worst of the crisis if you had enough bonds to cover five years of expenses?

Maybe. But maybe not.

Most retirement calculators assume your assets grow steadily—something like 7% per year. But in reality, markets don’t behave that way. A prolonged downturn could mean years of little to no growth, and those lost years aren’t easily recovered.

What If JPY Currency Suddenly Goes Up in Value?

This is a very real concern for me, and it’s tightly coupled with the financial crisis risk.

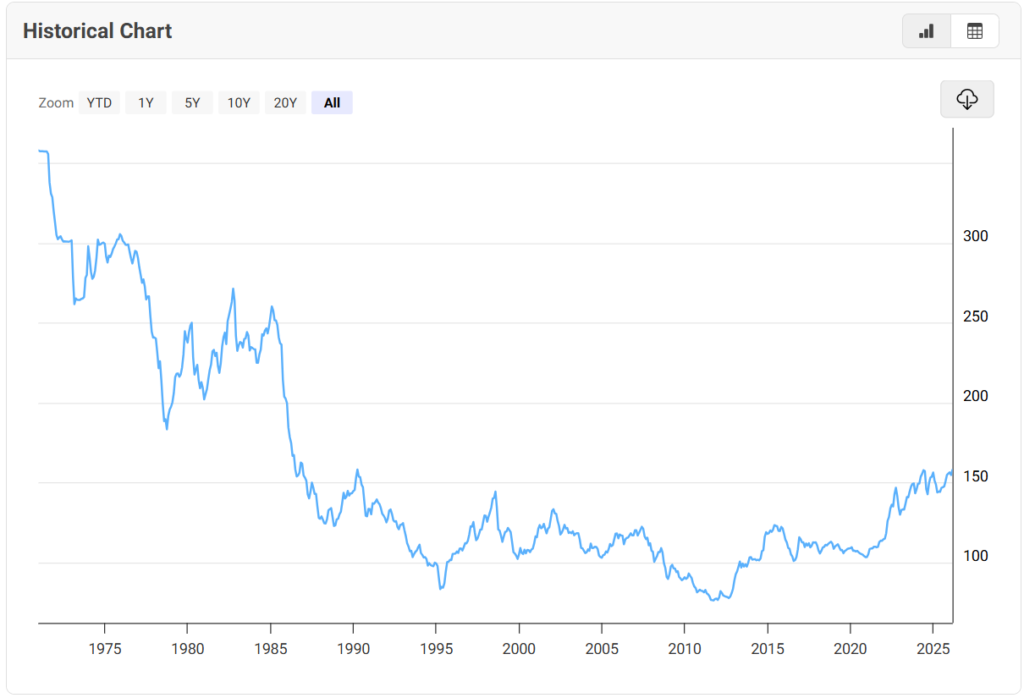

During the 2008 recession, the Japanese yen strengthened significantly. I remember when $1 USD was only worth around 80 JPY, and Japan felt like an expensive place to live.

If you look at historical trends, the yen tends to strengthen during global downturns, while the USD weakens. Only after the recovery does the USD regain strength.

Right now, $1 USD is around 155–160 JPY. But what if that reverses?

This is where things get scary.

I’m not just betting on the stock market, but also betting on exchange rates.

If a financial crisis happens, it could hit me twice:

- My assets lose value

- My living expenses (in USD terms) increase

At the same time.

So… Can I Really Retire at 39?

While the numbers say I can retire at 39, the reality is more complicated.

On paper, everything works.

But once you factor in market crashes and currency risk, the margin for error feels much smaller than it looks.

I’m not giving up on this plan, but I’m also not ready to trust the calculator blindly.

In Part 2, I will simulate how my current portfolio will perform under 2008 financial crisis.